Attention business owners! A significant regulatory change is on the horizon, and it’s one you can’t afford to ignore. Starting January 1, 2024, nearly all businesses operating in the United States will be required to file a Beneficial Ownership Information (BOI) report with the Financial Crimes Enforcement Network (FinCEN).

What is Beneficial Ownership?

Simply put, it’s about identifying the individuals who ultimately own or control your business, not just those listed on legal documents. This includes those with 25% or more ownership or significant control over voting rights or management decisions, such as corporate officers or directors.

Who needs to file?

The BOI requirement applies to most businesses, including:

Corporations

Limited

Liability Companies (LLCs)

Registered

Foreign Branches

Certain

trusts and other business entities

Basically if you have any business entity registered with your state, local, or tribal government, you will likely be required to file a Beneficial Ownership report.

What information needs to be filed?

For each beneficial owner, you’ll need to provide:

Name

and date of birth

Address

Social

Security Number (SSN) or Individual Taxpayer Identification Number

(ITIN)

Citizenship

and country of residence

Percentage

ownership or control

How and when do you file?

Filing will be done electronically through FinCEN’s secure online portal. There are two deadlines to keep in mind:

Companies

formed before January 1, 2024: Have

until January

1, 2025 to

file their initial report.

Companies

formed after January 1, 2024: Must

file within 30

days of

formation.

Anytime any of the reportable information changes (e.g. the business gets a new address or owner), a new report must be filed to inform FinCEN of that change.

Why does this matter?

The BOI rule aims to combat financial crime and money laundering by increasing transparency around who owns and controls businesses. This can help law enforcement investigate suspicious activity and prevent illicit actors from using shell companies to hide their tracks.

What should you do now?

FinCEN has not yet finalized the online Beneficial Ownership report, but beginning January 1, 2024, you will be able to file such a report. Make sure to do so by the appropriate deadline for your business.

Don’t wait until the last minute! Take action now to ensure you’re compliant with the Beneficial Ownership Information rule and avoid potential penalties. Remember, transparency is key, and compliance is crucial for your business’s reputation and legal standing. Willful failure to file the Beneficial Ownership report can subject the beneficial owner of the business to a civil penalty of $500 for each day the violation continues, as well as criminal penalties that include a $10,000 fine and 2 years in prison.

When it comes to filing taxes in

the United States, we usually hear about federal income taxes and

state income taxes, but we rarely hear about local income taxes.

Compounding the problem is the fact that most tax preparation

software and even some professional accountants rarely focus on local

income taxes, which may lead to unexpected tax surprises, or, even

worse, penalties and interest years later. Adding to the complexity

is the fact that different localities use different tax bases, with

some only taxing earned income, and others only taxing interest and

dividends as well as the fact that in some states, local income taxes

are reported on state income tax returns, while in others they must

be filed separately.

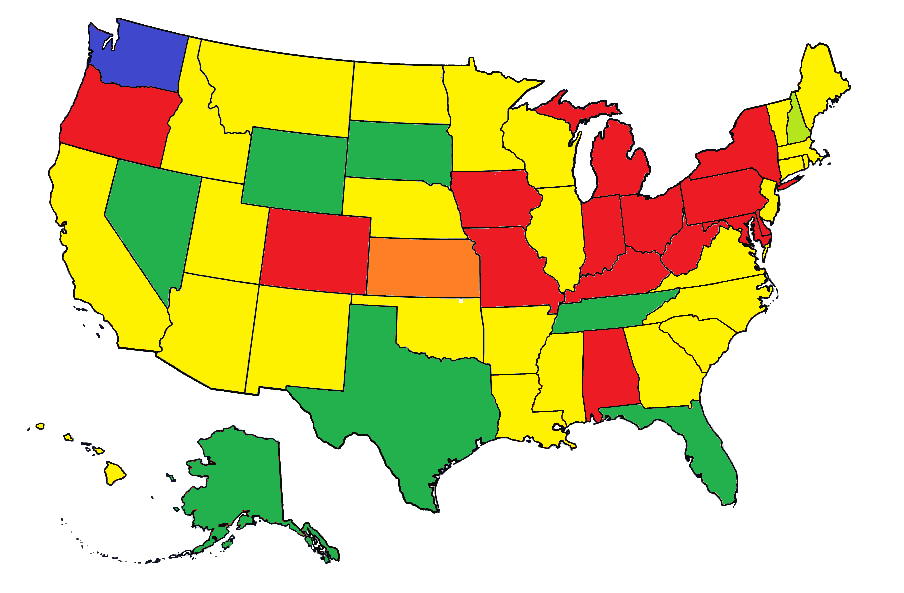

For your convenience, we have broken down this article by states that allow local income taxes. The states are not in geographical, rather than alphabetical order, going from east to west. Note that the purpose of the articles is purely informational and should not be taken as tax advice. A&M Logos International assumes no responsibility for the accuracy of the information provided.

If you have questions about filing local income taxes or need assistance with preparing federal, state, or local income tax forms or obtaining US tax residency certification, please contact us at (212) 233-7061 or e-mail us at info@apostille.us. You may also wish to visit our website.

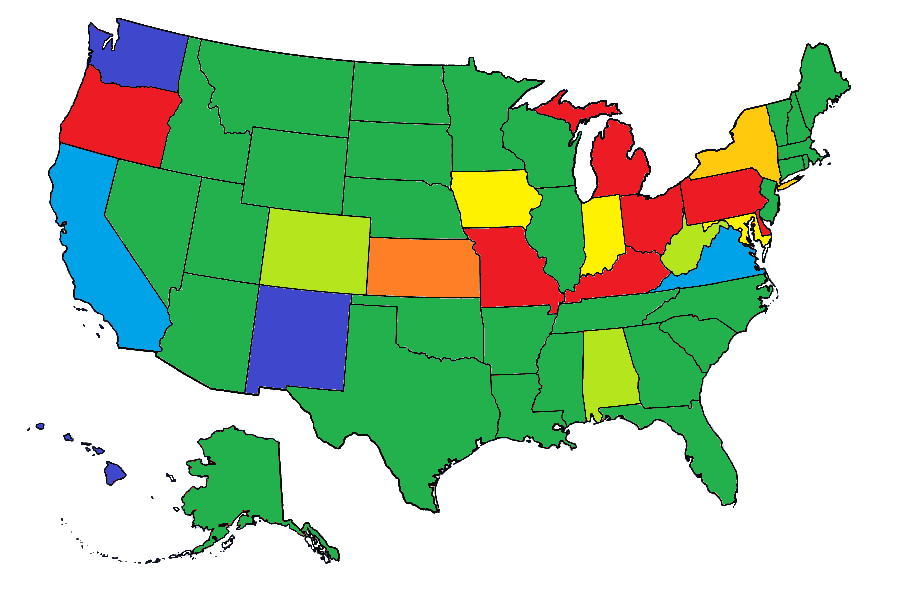

Green: No local income taxes Light Green: Local income taxes withheld by employer usually with no individual filing requirement Yellow: Local income taxes included on standard income tax form Gold: Local income taxes included on standard income form, with separate filing with city for self-employment income over a certain threshold as well as nonresident wage earners (currently only New York) Orange: Local income taxes on interest and dividend income only (currently only Kansas) Light Blue: Local business income taxes for self-employed individuals Dark Blue: State and local business taxes Red: Local income taxes must be filed separately with locality or local income tax collector (some jurisdictions require filing only if local income tax is not fully withheld by employer; others have mandatory filing for all residents)

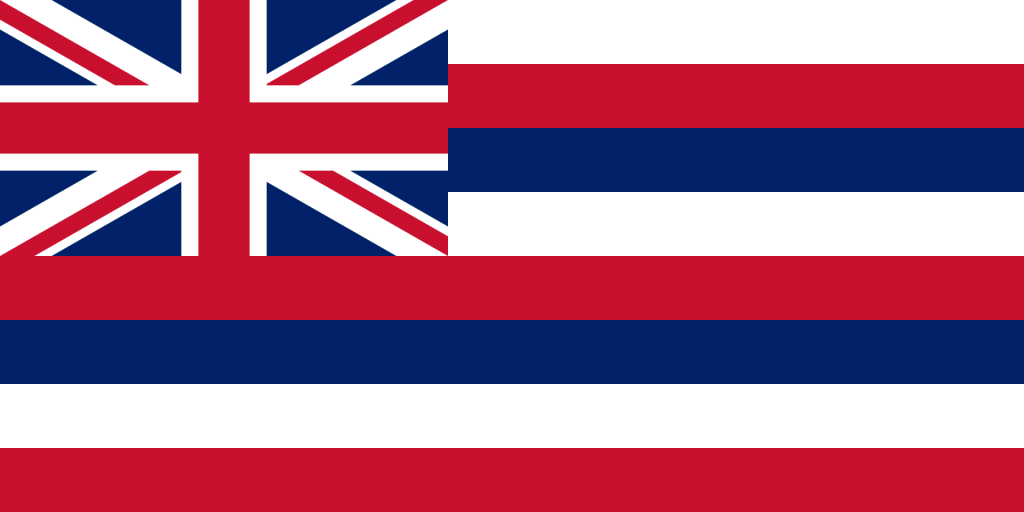

New York: The Empire State of Local Income Taxes

Flag of the State of New York

The

State of New York has 3 different local income taxes—New York City

income tax, Yonkers income tax, and the Metropolitan Commuter

Transportation Mobility Tax. All 3 taxes are collected on the

standard state income tax form (IT-201 for residents or IT-203 for

non-residents and part-year residents). If you changed your New York

City or Yonkers residence status, you would also need to file Form

360.1.

New York City only imposes an income tax on individuals who are residents of New York City. If you do not live in New York City but earn income within the city, you are not subject to the New York City income tax, unless you are employed by New York City (in which case you would have section 1127 income withheld from your paycheck and would need file Form 1127 with New York City).

Yonkers, on the other hand, subjects both residents and non-residents to the city’s income tax. If you are a resident of Yonkers, you can calculate Yonkers income tax on the New York State income tax return. If you are a non-resident with Yonkers-sourced income, you would also need to file Form Y-203 with your New York State income tax return.

It

is worth noting that New York City uses a wide income tax basis for

taxable income, including both earned and unearned income. Yonkers

residents are subject to a surcharge on the income tax paid to New

York State, while non-residents are only taxed on wages and

self-employment income earned in Yonkers.

Finally, the Metropolitan Commuter Transportation Mobility Tax is only imposed on self-employment income in excess of $50,000 sourced from New York City, as well as Nassau, Suffolk, Westchester, Rockland, Putnam, Dutchess, and Orange counties. It is also a payroll tax payable by employers operating within that area (the Metropolitan Commuter Transportation Mobility District) and is used to finance the Metropolitan Transit Authority (MTA).

It is also worth noting that self-employed individuals and unincorporated businesses sourcing income from New York City may also be required to file New York City Form 202, New York City Unincorporated Business Tax return, if their self-employment income exceeds $95,000.

Pennsylvania: Many Local Taxes, One Commonwealth

Flag of the Commonwealth of Pennsylvania

The

vast majority of Pennsylvania cities and school districts impose a

local income tax. It is important to note that all localities except

the City of Philadelphia are governed by Pennsylvania Act 32.

Act 32 municipalities and school districts are allowed to levy a Local Earned Income Tax. It is important to bear in mind that Local Earned Income Tax is included on the Pennsylvania State income tax return (Form PA-40), but must be filed with the local earned income tax collector. A local earned income tax collector is a private company authorized by a given county to collect local earned income taxes for municipalities and school districts within that county. Each county except Allegheny County has one tax collector for the entire county. Allegheny County (which includes the City of Pittsburgh) is split into 4 tax collection districts and currently uses 2 tax collectors (Jordan Tax Service and Keystone Collections Group).

To determine which tax collector collects taxes for your locality, you may wish to use an address lookup tool provided by the Pennsylvania Department of Community & Economic Development. It is crucial to remember to file your local earned income tax return with your local earned income tax collector as failure to do so will result penalties and interest years down the line. Pennsylvania employers must generally withhold local earned income tax based the higher rate of where you live or work, but you must still file at the end of the year to avoid getting penalized for failure to file. Since the tax is always a flat rate (PA law essentially prohibits progressive or regressive taxation), there would generally be no additional tax liability or refund if your employer fully withheld the tax due. If your employer does not withhold local earned income tax, you must make sure to file those tax remittances with the local earned income tax collector on a quarterly basis.

Bear in mind that Pennsylvania employers must also withhold another local taxed known as a Local Services Tax. The Local Services Tax is a flat annual fee, which is generally limited to $52 per year (with the exception of “financially distressed municipalities” which can collect more). The Local Services Tax is generally collected by splitting the annual fee into payroll periods and then withholding the tax from each paycheck (e.g. if payroll is done a weekly basis, a $52 will be split into 52 equal payments of $1 collected from each weekly paycheck until the end of the year). Individuals can apply for a refund of their Local Services Tax collected if their total earned income is below a certain limit (generally $12,000). Note that unlike the local earned income tax, local services tax are always paid to the municipality in which an individual does their work (rather than resides), although residence can be a factor in the cases of multiple employers. The local earned income tax collector often also collects local services tax for the same jurisdiction, but that is not always the case.

Pennsylvania is also unique in that some municipalities also impose a flat-fee occupational tax based on the locality’s assumption of the income you would be making from your job, and per capita tax, levied for the privilege of remaining alive withing a given locality. Note that individuals with low income can generally apply for an exemption from these taxes. Collection of these taxes is sometimes, but not necessarily handled by local earned income tax collectors.

Flag of the City of Philadelphia

The aforementioned taxes do not apply to the City of Philadelphia, which administers its own income tax system. Wage earners working in Philadelphia generally have PhiladelphiaWage Tax withheld from their paycheck. If the employer fully withheld Philadelphia Wage Tax, there is no filing requirement at the end of the year, unless the taxpayer wants to apply for a refund (generally applicable if the individual receives less than the federal poverty level).

Philadelphia residents who did not have Philadelphia Wage Tax withheld from their wages must register an account to pay Philadelphia Earnings Tax on a quarterly basis. At the end of the year, you would need to file an Annual Reconciliation of Employee Earnings Tax return with the City of Philadelphia.

Philadelphia also taxes certain unearned income such as interest, dividends, and rental income, and capital gains, so if you have those items of income, you would be required to file a Philadelphia School Income Tax return.

Finally, if you are a Philadelphia resident with self-employment income (from any source) or have Philadelphia-sourced self-employment income, you would need to register as a business and file a Net Profits Tax return with the City of Philadelphia. Gross receipts (i.e. income without any deductions) from Philadelphia-sourced self-employment are also subject to the Philadelphia Business Income & Receipts Tax. If your income is below the threshold, you would still need to file a “No Tax Liability” tax exemption form. It is important to underscore that Philadelphia Net Profits Tax (NPT) and Business Income & Receipts Tax (BIRT) are 2 separate taxes on self-employment income, although a partial credit can be applied to NPT for BIRT previously paid.

Delaware: The First State and the Lone Local Tax

Flag of the State of Delaware

The only locality to have an income tax in the State of Delaware is the City of Wilmington. If you are employed by a Delaware employer and are a resident of Wilmington or you are a non-resident of Wilmington but work in the city, your employer would be required to withhold Wilmington Earned Income Tax, in which case you would not need to file any return at the end of the year. If, however, you are a Wilmington resident and your employer does not withhold Wilmington Earned Income Tax (as could be the case if you live in Wilmington but work out of state), you would need to set up a self-reporting employee earned income taxpayer account and file and pay Earned Income Tax with the City of Wilmington on a quarterly basis.

If you are a resident of Wilmington with self-employment or rental income (as well as certain business-related capital gains) or you have those items of income sourced from Wilmington, you would need to file a Wilmington Net Profits Tax return to pay Wilmington Net Profits Tax.

Maryland: A County-by-County Tale

Flag of the State of Maryland

All counties of Maryland as well as the City of Baltimore impose a Local Income Tax on the same items of income as the State of Maryland. Local Income Tax in Maryland is levied by the county (or independent city) in which you reside. It is calculated and reported on the Maryland resident income tax return (Form 502).

If you are not a resident of Maryland, you would generally not be liable for local income taxes, which is why local income tax is not included on the Maryland non-resident income tax return (Form 505). However, if you are a resident of a local jurisdiction in New York, Pennsylvania, Delaware, Alabama, Kentucky, Ohio, Michigan, Indiana, and Missouri that imposes an income or earnings tax on residents of Maryland, you must file Maryland Form 515 to calculate your Maryland local income tax liability.

Virginia: A Commonwealth of Local Business Taxes

Flag of the Commonwealth of Virginia

The Commonwealth of Viginia does not have local income taxes per se, but self-employed individuals may be required to register with the county or independent city from which they derive their self-employment income. Many counties and independent cities exclude gross receipts below $10,000 from local Business License Tax. Note that some counties and independent cities may also require the filing of a personal business property tax return.

While you may think you can get away with not registering your self-employment activities, you may wish to consider the fact that the Virginia Department of Taxation provides information on individuals who filed Federal Schedule C to independent cities and counties. This informational exchange is pretty new and will often not be of concern to those who received less than $10,000 in gross receipts. However, it is always a good idea to check registration requirements and fees with your independent city or county.

Alabama: A Local Twist

Flag of the State of Alabama

A number of cities in Alabama require employers to withhold a Local Occupational Tax (a flat percentage tax) from each paycheck paid to employees. The tax is paid on income sourced from the municipality imposing the tax. This tax is generally not refundable and there is no obligation on the part of individuals to file this tax (unless they are employers).

Kentucky: Local Taxes Galore

Flag of the Commonwealth of Kentucky

Most counties and municipalities, as well as some school districts (usually sharing boundaries with their respective counties), impose local income taxes on income earned withing that particular jurisdiction. For school districts, the rate varies depending on whether the individual earning the income is a resident of that school district or not. For counties and municipalities, on the other hand, the rate generally does not vary based on residence status.

Employers are required to withhold the local income tax, often known as Occupational License Tax or Occupational Tax from the paychecks of their employees. Employees are generally not required to file any tax returns at the end of the year.

At the same time, if you had self-employment income or certain rental income sourced from a given Kentucky county, school district, or municipality, you would generally need to register with that jurisdiction to file and pay the income tax, which in these scenarios is often referred to as the Net Profits Tax (but sometimes the same name—Occupational License Tax or simply Occupational Tax—may be used in reference to self-employment). In some cases, like the consolidated Louisville/Jefferson County Metro or Lexington-Fayette Urban County, it is sufficient to file 1 return. In other cases, 2 or even 3 different returns may need to be filed. For example, an individual with self-employment income from Bowling Green, would need to register and file 3 separate Net Profits Tax returns with Warren County, the Warren County Public School District, and the City of Bowling Green.

It is worth bearing in mind that as a W-2 salaried employee, you should generally not be worried about any local income tax filings in Kentucky. However, if you are self-employed, you should be aware that many Kentucky cities, counties, and school districts require payers of non-employee income to report those payees. Payees that fail to register and file with the respective county, school district, and/or municipality will be subject to penalties and interest on their unpaid occupational license / net profits tax.

West Virginia: City Services Fee

Flag of the State of West Virginia

Some West Virginia municipalities require employers to withhold a flat City Services Fee from paychecks of employees. The tax is a flat fee deducted from employee paychecks on a weekly basis (e. g. $3 per week as is the case for Charleston). Employees with multiple employers should make sure to inform their new employer that their first employer is already withholding the City Services Fee to avoid having the fee withheld twice. In some cities, employees may also qualify for a refund of the fee if they get charged the same tax more than once by multiple employers. No end-of-year tax return filing is required.

Ohio: Municipal and School District Income Taxes

Most municipalities in Ohio impose a Municipal Income Tax on income earned in that municipality as well as on any income earned by residents of that municipality. Local employers must generally withhold local income tax from the salaries of resident and non-resident employees. Generally, only earned and certain rental income is subject to local income tax.

Many Ohio municipalities, such as Columbus, Cincinnati, and Toledo, collect their income taxes directly. Some municipalities (e.g. Columbus, Cincinnati) only require individuals to file if their income tax was not fully withheld by their employer. Others impose a filing requirement on anybody with earned income or on any adult resident independent of income.

A number of Ohio municipalities do not collect their income tax directly but use the services of 1 of 2 tax collection agencies—the Regional Income Tax Agency (RITA) or the Central Collection Agency (CCA). RITA generally collects for some small to mid-sized municipalities spread out throughout Ohio, while CCA primarily collects for municipalities in the Cleveland metropolitan area, including Cleveland itself.

In addition to municipal income taxes, Ohio also allows school districts to levy an income tax. Ohio School District Income Tax is collected by the state, but it is not included on the standard state income tax return (Form IT 1040). A separate form, SD 100, must be filed with the State of Ohio if you are subject to the tax. It is worth bearing in mind that only some school districts impose the tax, so many Ohio residents do not have to worry about filing Ohio Form SD 100. School districts can pick whether to use a traditional tax base (generally all items of income taxed by the State of Ohio) or an earned income tax base. It is also worth remembering that School District Income Tax is only imposed on residents of that school district.

Michigan: City Income Tax

Flag of the State of Michigan

A number of Michigan cities impose a City Income Tax on both residents and non-residents with income sourced from that city (the rate for residents is usually higher). The income tax base is generally quite wide, so any income taxable by the State of Michigan would usually be taxable by a city imposing the income tax as well.

City income taxes are generally collected by the individual cities themselves. Individuals residing in those cities or having income sourced from those cities must generally file a city tax return if their income exceeds a certain threshold. The only city that does not collect its own income tax is Detroit, whose income tax is collected by the State of Michigan. It is not, however, reported on the standard Michigan income tax return (Form MI-1040), but on the State-issued Detroit Resident Income Tax return (Form 5118) or Detroit Non-Resident Income Tax return (Form 5119).

Indiana: County-Level Tax

All Indiana counties have a Local Income Tax imposed on both residents and non-residents with income sourced from that county. The county income tax is reported on the standard Indiana state income tax return, Form IT-40 for residents or Form IT-40PNR for non-residents and part-year residents.

Iowa: School and Emergency Medical Services Surtax

Flag of the State of Iowa

Many Iowa school district impose a School District Surtax on tax due to the State of Iowa on residents of that school district. In addition, Iowa allows counties to impose an Emergency Medical Services (EMS) Surtax. Appanoose County is currently the only county imposing the county surtax. These surtaxes are calculated on the standard Iowa State Income Tax return (Form IA 1040).

Missouri: Show Me the Earnings Taxes!

Flag of the State of Missouri

Missouri law allows the 2 largest cities of the state to impose local income taxes—St. Louis and Kansas City. In both cities, the tax can only be imposed on earned income and is known as the Earnings Tax. Residents of St. Louis and Kansas City are subject to the tax on income earned anywhere, while non-residents must only pay the Earnings Tax on income earned in St. Louis or Kansas City.

Taxpayers are not required to file any tax returns with their cities if their employer fully withholds the Earnings Tax (currently at 1% in both cities). If Earnings Tax is not fully withheld, as is often the case with individuals residing in St. Louis or Kansas City but working out of state, those individuals must file an Earnings Tax return with their respective cities. In St. Louis, that form is known as Form E-1, while in Kansas City it is called Form RD-109.

Kansas: Only Intangibles Taxed Locally in Sunflower State

Flag of the State of Kansas

The Sunflower State allows counties and municipalities to impose a local income tax on interest and dividends only. This is known as the Kansas Local Intangibles Tax. The tax is generally imposed on residents of a particular municipality or county if that locality imposes a local intangibles tax and the individual in question receives interest or dividend income. In certain cases, if the interest and/or dividend income is derived from property or business located in a locality imposing the tax, non-residents would also need to file and pay the tax.

Individuals owing Local Intangibles Tax in excess of $5 must file and pay the Local Intangibles Tax on State Form 200. Note that even though the form is issued by the state, it must the filed with the county tax collector where the tax is owed.

Colorado: Occupational Privilege Taxes in the Centennial State

Flag of the State of Colorado

Colorado allows municipalities to impose a flat-fee Occupational Privilege Tax, which is withheld by an employer from an employee’s paycheck. The Occupational Privilege Tax applies only to earnings made in the municipality imposing the tax and is not based on residence.

An employee would generally need to certain minimum amount to be subject to the Occupational Privilege Tax. For example, the City of Denver imposes an Occupational Privilege Tax of $5.75 per month payable by an employee (a corresponding $4 per month must be paid by the employer for each employee). The Denver Occupational Privilege Tax only applies if the employee received compensation of at least $500 in that month.

While most municipalities imposing the Occupational Privilege Tax provide for a minimum monthly income that must be met for the tax to be imposed, this is not always the case. For example, the City of Sheridan imposes a $3 per month Occupational Privilege Tax on any employee working in the city (with a corresponding employer payment of $3).

Individuals are generally not required to file any returns, but employees should be cognizant of the tax in the case of having multiple employers, as new employers may not be aware that the required tax is already being withheld.

New Mexico: Self-Employed Beware of the Gross Receipts Tax!

Flag of the State of New Mexico

New Mexico does not have local income taxes per se, but most self-employed individuals are required to register for and file the New Mexico Gross Receipts Tax, which is often equated with a sales tax, as it can be passed on to the final consumer (although final liability for its payment lies with the business or self-employed individual). Note that unlike sales taxes in other states, most services are subject to New Mexico Gross Receipts Tax. And because of a tax information exchange program between the IRS and New Mexico, the State will find out that you filed a Schedule C sooner or later and, like it or not, send you a penalty notice if you have not registered and filed the appropriate forms.

The local component of the Gross Receipts Tax is calculated when filing Form TRD-41413 (the New Mexico Gross Receipts Tax return) with the State. Individuals are required to register by filing Form ACD-31015 with the State of New Mexico when they start engaging in or deriving income from self-employment.

California: Business Tax Traps for the Self-Employed working in the Municipalities of the Golden State

Flag of the State of California

California does not impose any local income taxes per se, but many municipalities require self-employed individuals to obtain a Municipal Business Tax Certificate, or Business License, which generally requires payment of a business license fee or business tax. Some counties may also have a business tax or license requirement, especially for those in unincorporated areas of the counties.

In some municipalities, individuals with gross receipts or earnings below a certain threshold can apply for an exemption (e. g. in the City of Los Angeles, the “small business exemption” exempts self-employed individuals with gross receipts under $100,000 from paying the business tax, but those individuals must apply for an exemption on time).

Note that that the deadline to pay business license fees or to apply for an exemption is often earlier than the regular tax filing deadline. Self-employed individuals must generally register when they start engaging in business, however. Also, bear in mind that California municipalities and counties can easily find out if you have filed a Schedule C because of a tax information program with the California Franchise Tax Board.

Oregon: A Wild Mishmash of Local Taxes in the Beaver State

Flag of the State of Oregon

While the State of Oregon is one of the few states that does not have a sales tax at either the state or local level, Oregon has a multitude of crisscrossing and overlapping local income taxes, particularly in the Portland and Eugene metro areas.

First of all, in addition to Oregon State Income Tax, residents of Oregon and non-residents of Oregon working in the state are subject to the Oregon Statewide Transit Tax aimed at funding public transit services in the state. Residents of Oregon who work for an out-of-state employer who does not withhold that tax must pay the 0.1% tax by filing Oregon State Form OR-STI.

All individuals aged 18 or older who live in the City of Portland are subject to a $35 per person flat-fee Arts Tax aimed at financing arts education in the city. These individuals must file an Arts Income Tax return with the City of Portland. Individuals who earn less than $1,000 per year or are part of a household making less than the federal poverty level are exempt from paying the $35 Arts Tax, but must still qualify for the exemption by filing the Arts Income Tax return with the city.

The City of Portland also collects 2 local personal income taxes, both of which to single or married filing separately individuals earning over $125,000 per year (the threshold is increased to $200,000 a year for married filing jointly households as well as heads of household or qualifying surviving spouses). The income base for both taxes is wide, coinciding with Oregon’s definition of taxable income and includes both taxable and non-taxable income.

The first local income tax is known as the Metro Supportive Housing Services (SHS) Personal Income Tax and is a 1% tax applicable to income made over the filing threshold by residents of the area within the jurisdiction of the Portland Metro, a regional government (the only regional government in the United States) that encompasses the City of Portland as well as other areas of Multnomah, Clackamas, and Washington counties outside of Portland (but not the entire counties). The tax also applies to non-residents having income sourced from the Portland Metro in excess of the threshold. Metro Residents with income in excess of the filing threshold must file Portland Form MET-40, while non-residents with Metro-sourced income in excess of the threshold must file Portland Form MET-40-NP. The forms must be filed with the City of Portland. The tax is used to finance shelters and other housing services for individuals facing homelessness.

The second local tax is known as the Multnomah County Preschool For All (PFA) personal income tax and is a 1.5% tax applicable to income made over the filing threshold by residents of the entirety of Multnomah County. The tax also applies to non-residents having income sourced from Multnomah County in excess of the threshold. Multnomah County residents with income in excess of the threshold must file Portland Form MC-40, while non-residents with income sourced from Multnomah County above the threshold must file Portland Form MC-40-NP. As with the Metro SHS tax, both form are filed with the City of Portland.

The City of Portland provides an

option to file a combined Metro SHS and Multnomah County PFA tax

return online.

Individuals who are self-employed face an additional layer of complexity with regard to local income taxes in Oregon.

First of all, self-employed individuals making over $400 a year in the Tri-County Metropolitan (TriMet) Transportation District (the public transit district that services the Portland metropolitan area covering Multnomah, Clackamas, and Washington counties) or the Lane County Mass Transit District (the public transit district that services the Eugene metropolitan area covering Lane County) must file and pay an additional self-employment transit tax. Note that the boundaries of the districts do not necessarily coincide with the boundaries of the counties they service and are subject to change.

TriMet Transportation District Self-Employment Tax must be reported on Oregon State Form OR-TM, while Lane County Mass Transportation District Self-Employment Tax must be reported on Oregon State Form OR-LTD. Both forms are filed with the State of Oregon.

If your self-employment income is derived from the City of Portland and/or Multnomah County, you would also be subject to the City of Portland Business License Tax and/or Multnomah County Business Income Tax. Both the City of Portland and Multnomah County provide exemptions for gross income from all sources below a certain threshold ($50,000 for Portland and $100,000 for Multnomah County). Both taxes must be filed on Portland Form SP (Combined Tax Return for Individuals) with the City of Portland. In order to file the form, a self-employed individual would first need to register as a business with the City of Portland.

Self-employed individuals with income in excess of $5,000,000 derived from Portland Metro must also pay an additional 1% Metro SHS Business Income Tax. It appears that the tax can currently only be paid online, although it appears that the City of Portland may also issues a standalone Metro SHS Business Income Tax form in the future.

Finally, individuals with self-employment income in excess of $400 per year sourced from the City of Eugene must file and pay the City of Eugene Self-Employment Tax. The tax is a counterpart to the Eugene Community Safety Payroll tax aimed at financing local law enforcement. The tax is filed of City of Eugene Form EUG-SE. Individuals must first register as a business via the online MuniREVS resource to be able to file the tax return.

Washington: No Income Tax, but the Self-Employed must beware the B&O Tax

Flag of the State of Washington

The State of Washington has no local (or state) income tax per se (although a state-level capital gains tax on certain long-term capital gains was implemented in 2021). However, individuals who are self-employed must be aware of the Washington Business & Occupation (B&O) Tax, which is imposed on gross income (i. e. your income without the deduction of any expenses, such as labor, materials, taxes, or fees) sourced from the State of Washington. The tax rate varies depending on the exact type of business. If you are self-employed, your business will likely fall under the services category, which has a rate of 1.5% of gross income (increased to 1.75% if the previous year’s gross income attributable to the activity was $1,000,000).

Note that you are not required to register with the State of Washington if your Washington-sourced self-employment gross income is under $12,000. It is therefore vital to monitor your revenue throughout the tax year. As soon as you hit the $12,000 mark, you would need to file a Business License Application (Form 700 028) with the State and pay the registration fee (currently $50).

If your self-employment is carried on within the boundaries of a particular Washington municipality, that municipality may also require you to obtain that municipality’s business license and pay the registration fee. The State of Washington provides a City and County Addendum (Form 700 060) to their state Business License Application for many (but not all) Washington municipalities.

Some municipalities, most notably Seattle, have a separate process for business registration. If you register with the state, it is also a good idea to register with the municipality in which you conduct your self-employment.

If you conduct your self-employment activities in an unincorporated area of a given Washington county, you may need to register and pay the business license fee with the county. The State of Washington collects the fee only for Asotin and Franklin Counties (currently $25 and $150, respectively). Many, but not all, counties do not require self-employed individuals to register or pay a business license fee.

If you register with the State, you would generally be required to file a Combined Excise Tax on annual, quarterly, or monthly basis (depending on your total gross income). The return is used to calculate and pay the B&O Tax owed.

If you registered with a municipality, you would also generally be expected to file a municipal business tax return. However, many municipalities provide an exemption for the Municipal B&O Tax to come into play. For example, in Seattle that exemption is $100,000, so self-employed individuals with gross annual income below the exemption would not need to pay any municipal B&O tax but would still need to file a municipal business income tax return.

Hawaii: Aloha General Excise Tax for Self-Employed and Renters

Flag of the State of Hawaii

The Aloha State does not have local income taxes per se, but most self-employed individuals are required to register for and file the Hawaii General Excise Tax, which is often equated with a sales tax, as it can be passed on to the final consumer (although final liability for its payment lies with the business or self-employed individual).

Note that unlike sales taxes in other states, most services are subject to the Hawaii General Excise Tax. Also, unlike the New Mexico Gross Receipts Tax (which, in many ways is very similar to the General Excise Tax), Hawaii also classifies rental income (reported on Federal Form 1040, Schedule E) as income subject to the General Excise Tax). Hawaii counties may also impose a County General Excise Tax surcharge. A 0.5% surcharge is currently imposed in Honolulu, Kauai, Hawaii, and Maui counties (there is currently no surcharge in the remote Kalawao County). The Hawaii General Excise Tax and county surtaxes are paid to the State of Hawaii on State Form G-45 (note that you would first need to register your business and obtain a Hawaii Tax ID by filing Form BB-1).

Green: States with no income tax Light green: States with income tax on interest and dividends only (currently only New Hampshire) Blue: States with income tax on certain long-term capital gains only (currently only Washington) Yellow: States with state income tax, but no local income taxes Orange: States with state income tax and local income taxes on interests and dividends only (currently only Kansas) Red: States with state and local income taxes

Tax residency is a concept that lies at the core of an individual’s tax obligations. For most people, it’s relatively straightforward: you reside in a particular place, and that place’s tax laws apply to your income. However, the nuances of tax residency become considerably more complex when you factor in multiple states and the influence of mutual tax treaties. Each state in the United States has its own rules for determining tax residency, and these rules can significantly impact an individual’s tax liability. This article explores the intricacies of state-level tax residency rules, mutual tax treaties, and the challenges individuals face when dealing with multi-state taxation.

State-Level Tax Residency Rules

Each

state has its own set of rules for determining tax residency. While

there are some commonalities, such as the general notion that

residency is based on where you live, important differences exist.

Here are some key factors that states often consider:

1.

Domicile vs. Statutory Residency: Many states distinguish between

domicile (where you intend to make your permanent home) and statutory

residency (where you spend a significant portion of the year). Some

states may consider you a resident if you maintain a domicile within

their borders, even if you spend most of your time elsewhere.

2.

Physical Presence: The number of days you spend within a state’s

borders is a common factor in residency determinations. States may

have different thresholds, such as 183 days or more in a tax year.

3.

Home Ownership or Rental: Owning or renting a home in a state can be

a factor. Owning property in a state may suggest a stronger

connection to that state.

4.

Family and Business Ties: Having close family members or a business

in a state can also influence your residency status.

5.

Voting and Driver’s License: Registering to vote or obtaining a

driver’s license in a state can be viewed as evidence of residency.

Mutual Tax Treaties and State Residency

Muutal

tax treaties between states can further complicate the issue of tax

residency. These treaties are agreements between states that aim to

prevent double taxation and clarify residency rules for individuals

with ties to multiple states. They often provide criteria for

determining residency in cases of conflict between states.

However,

it’s essential to note that not all states have mutual tax treaties

with each other, and the provisions of these treaties can vary

widely. Therefore, individuals navigating multi-state taxation should

be aware of the specific treaties that apply to their situation and

how they may impact their tax liability.

Mutual

tax treaties play an important role in the case of individuals who

work in one state but reside in another.

For

example, since New York does not have any mutual tax treaties

governing reciprocity with any other states, individuals who work in

New York, but live in, for example New Jersey or Connecticut, must

still file a New York state non-resident income tax return (Form

IT-203) and then also file their state-s resident income tax return

(Form NJ-1040 in the case of New Jersey or Form CT-1040 in the case

of Connecticut), taking a tax credit for the taxes already paid to

New York.

On

the other hand, New Jersey has a mutual tax treaty governing

reciprocity with Pennsylvania. Individuals who live in Camden, New

Jersey, but commute to Philadelphia, Pennsylvania, for work, do not

need to file a Pennsylvania personal income tax return (Form PA-40),

but must file a New Jersey tax return to report their income and pay

the entirety of the taxes owed. Pennsylvania employers would be

required to withhold New Jersey income tax for employees that reside

in New Jersey. That being said, the situation is further complicated

by the fact Pennsylvanian municipalities and school districts do not

adhere to the mutual tax treaty, so if we take the aforementioned

example, Philadelphia non-resident wage tax would still be withheld

(a tax credit for the tax withheld locally can also be claimed on the

New Jersey income tax return). While Philadelphia does not require

individuals to file a tax return if their employer fully withheld the

tax, low income taxpayers may benefit from filing a wage tax refund

petition with the city.

A

resident of Philadelphia working in Camden would also not need to

file a New Jersey income tax return, but the income received in New

Jersey would need to be reported on their Pennsylvania income tax

return. Also, unless their New Jersey employer voluntarily withholds

Philadelphia Wage Tax, they would need to register to file and pay

earnings tax with the city. If the individual resides anywhere else

in the Commonwealth of Pennsylvania, they will likely be required to

pay quarterly taxes to their local earned income tax collector

(collecting taxes for municipalities and school districts).

By

virtue of its status, the District of Columbia does not tax

non-residents, so individuals who live in Maryland or Virginia, but

commute to DC for work only need to file and pay taxes in their

respective states of residence. On the other hand, DC residents who

work in Maryland and Virginia only need to file and pay taxes in

Washington, DC.

There

are also some states that have unilateral tax treaties governing

reciprocity. For example, residents of California working in Arizona

do not need to file and pay Arizona taxes, but must report their

entire income on their California resident income tax return. Their

Arizona employers would need to withhold California taxes from their

salary. On the other hand, an Arizona resident working in California

would be required to file and pay California income tax. Their

California employers would only need to withhold California taxes

from their pay. Once they file their California taxes, they would

also need to file an Arizona resident income tax return, taking a tax

credit for the California taxes already paid.

Proving Non-Residency and Challenges

Proving

that you are no longer a resident of a particular state can be a

complex and challenging process. Some states may require

documentation such as lease agreements, utility bills, or sworn

affidavits to demonstrate your intent to change your domicile.

However, mere declarations may not always suffice, especially if you

maintain ties to the state, such as a vacation home or continued

business interests.

Additionally,

situations where individuals live in one state and work in another

can be particularly tricky. The

general rule of thumb is that states tax based on both residency and

source of income, although the aforementioned tax treaties outline

situations in which individuals only need to pay taxes to the state

in which they reside. Some localities also tax both residents and

individuals sourcing income from that jurisdictions, while others tax

only residents or only individuals/businesses sourcing income from

the jurisdiction.

Navigating the intricacies of these rules and ensuring compliance can

be a daunting task.

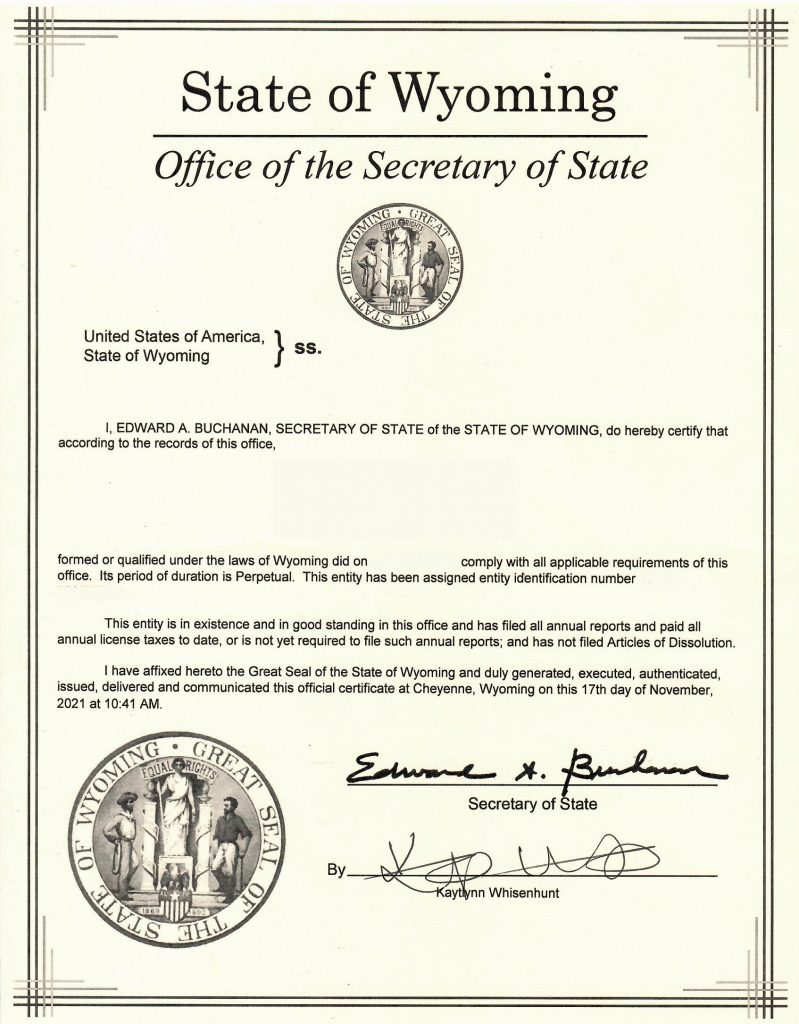

A

Certificate of Good Standing, sometimes known as Certificate of

Status or Certificate of Existence, is a state-issued document

confirming that a given business entity is in “good standing”

with the state. This means that the entity has been properly

registered with the state, is up to date on paying all required state

registration fees and taxes, has submitted all documents required to

be filed, and is legally permitted to engage in business in the

state.

Certificates

of Good Standing are typically issued by the state agency in charge

of regulating business activities in that state. In New York,

California, and Delaware, for example, the document is issued by each

state’s respective Division of Corporations (a division of each

state’s Secretary of State). In New Jersey, the responsible agency

is the Division of Revenue and Enterprise Services, part of New

Jersey Treasury.

One

prerequisite for obtaining a Certificate of Good Standing is to have

your business entity registered with your respective state. In many

states, sole proprietorships and independent contractors are not

required to register and therefore cannot apply for Certificates of

Good Standing.

Unlike

business licenses and permits, Certificates of Good Standing are

generally not required to conduct business in state. However, they

may be required if you are trying to open a business bank account,

set up credit and debit card processing systems, apply for a line of

credit on behalf of the business, or register as a “foreign entity”

in a state where the entity is not registered but engages in

business.

Many

foreign government agencies and regulators also require US-based

companies seeking to open subsidiaries to provide Certificates of

Good Standing to do so. In some cases, Certificates of Good Standing

need to be regularly renewed to demonstrate that the business

continues to remain in “good standing” with the state in which it

is registered by paying annual taxes and fees and filing the

requisite informational paperwork.

A&M Logos International has been assisting individuals and companies with retrieving and legalizing Certificates of Good Standing from all 50 states in the US. We know the ins and outs of the process with a particular focus on making sure the Certificate of Good Standing is valid for use abroad—by obtaining an apostille for Apostille Convention countries (e.g., India, Brazil, Germany) or undergoing the chain legalization process for non-Apostille Convention countries (e.g., Nigeria, Thailand, Vietnam). We can also provide a certified translation of the Certificate of Good Standing if necessary.

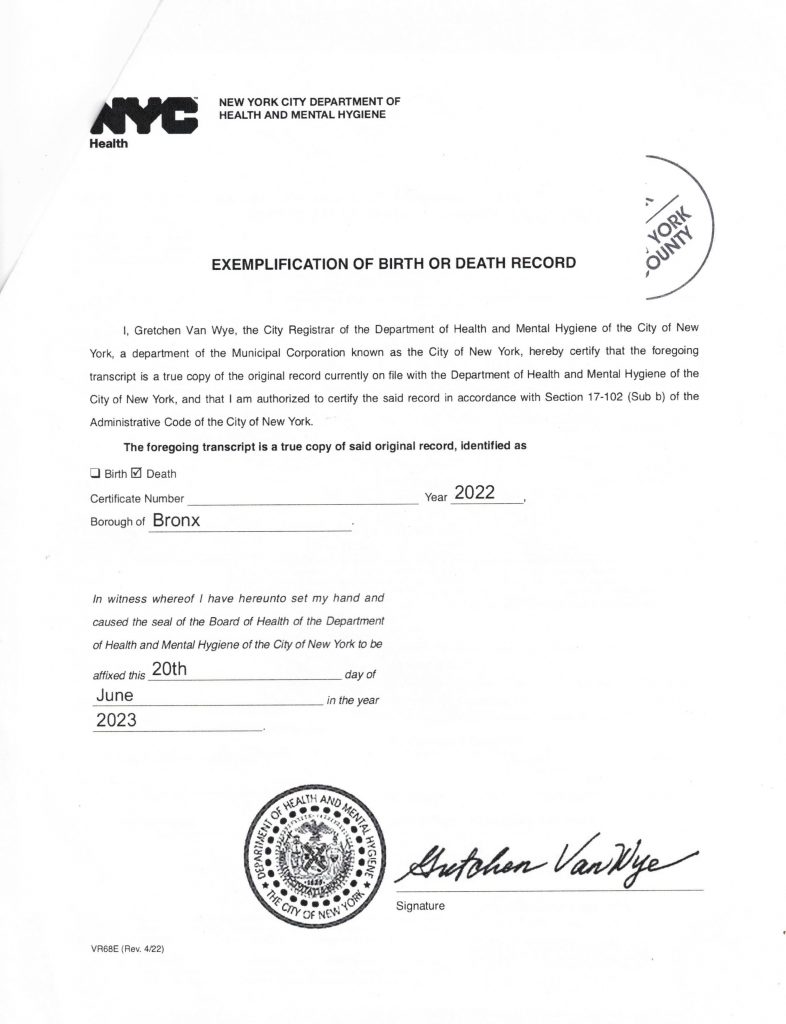

Sample Letter of Exemplification with the certificate number removed

We

are often contacted by people who were born in New York City or who

have had their loved ones pass away withing the 5 boroughs asking how

they could get the respective birth and death certificate apostilled

or authenticated for use abroad. A prerequisite for legalization is a

letter of exemplification, a statement signed by the New York City

Registrar confirming that the certified copy is indeed a true copy of

the original document.

In

New York City, birth and death certificates are issued by the New

York City Department of Health and Mental Hygiene. If you have the

original certificate or a certified copy without a letter of

exemplification, you would not be able to get it legalized for use

abroad, and would need to order another certified copy, making sure

to also request an accompanying letter of exemplification. If you are

applying by mail or in person, you would simply need to answer “yes”

to the question “Do you need a letter of exemplification?”. If

applying online via VitalChek, make sure to select “Apostille /

Authentication” as the reason for the application.

It

is usually advisable to apply online or, if you can get an

appointment, in person, as mail-in applications can take weeks, if

not months. With online applications, the certificate certified copy

and letter of exemplification typically arrives back in 2-3 weeks. If

you apply in person, you can typically get the certificate the same

day, but you would need to schedule an appointment beforehand.

Once

you receive your certificate and letter of exemplification, we would

be able to take care of getting your document apostilled or

authenticated for use abroad. We will first certify the certificate

with New York County, which is the only county that can certify the

signature of the City Registrar, even if the certificate itself was

originally issued outside of Manhattan. Once we get it certified with

the county, we would be able to get it apostilled or authenticated

with New York State. With regular service, the whole process of

getting county certification and state authentication takes about 4-8

weeks. With courier-expedited service, the process can usually be

done in under 1 week.

If

the destination country is not a member of the Apostille Convention,

the certificate would generally need to be further authenticated at

the federal level, after which we would legalize it with the target

country’s embassy or consulate. Federal authentication typically

takes at least 1 month, but sometimes be as long as 3 months, with no

option to expedite. Some countries, such as Vietnam, do not require

federal authentication. China requires federal authentication only

for documents issued in the jurisdiction of the Chinese Embassy in

Washington, DC.

Note

that New York City marriage certificate and divorce decrees do not

need to be accompanied by letters of exemplification. Certified

copies of marriage certificates are issued by the City Clerk, whose

signature is recognized by New York County, while divorce decrees are

typically obtained directly from the Clerk of the County in which the

divorce took place. We are able to retrieve these records ourselves,

although we would require you to provide us with a signed and

notarized letter of authorization (which we can prepare for you).

If

you have questions about New York City vital records, feel free to

call us at (212) 233-7061 or e-mail us at info@apostille.us.

In today’s interconnected world, individuals often seek educational opportunities in countries other than their own. Individuals immigrating to the United States often face the additional challenge of being able to use their educational credentials for the purpose of employment or further education in the United States. In some cases, US immigration authorities may also require foreign diplomas and other documents to be duly evaluated in their US equivalents for the purpose of visa and immigration applications. That is why evaluating your foreign diplomas or certificates can be a window to numerous opportunities.

Understanding Credential Evaluation

Credential evaluation is the process of assessing and comparing foreign educational qualifications to their equivalents in the United States. There are typically two main types of evaluations: document-by-document evaluations and course-by-course evaluations.

1. Document-by-Document Evaluations:

These evaluations provide a concise summary of the foreign diploma or degree, stating its equivalent in the U.S. education system.

They are a basic assessment, often used for general purposes like employment or immigration.

2. Course-by-Course Evaluations:

These evaluations provide a detailed breakdown of the foreign education, listing subjects studied, credits earned, and grades achieved.

They are typically required for further education, professional licensing, or employment in specialized fields.

Examples of Foreign Diplomas and Their U.S. Equivalents

To illustrate the importance of credential evaluation, let’s consider a few examples:

1. The Indian Bachelor of Technology (B.Tech):

In the U.S., this is often equivalent to a Bachelor of Science (B.S.) in Engineering.

A course-by-course evaluation would detail the specific engineering disciplines studied, such as electrical, mechanical, or computer engineering.

2. The Chinese Master’s in Business Administration (MBA):

This might be evaluated as a Master of Business Administration (MBA) in the U.S.

A course-by-course evaluation would outline the core business courses taken, like finance, marketing, and management.

3. The European Bachelor’s in Medicine:

This can be assessed as the equivalent of a Bachelor of Science (B.S.) in Medicine or a pre-medical degree.

A course-by-course evaluation would list the medical subjects studied, clinical training, and practical experience.

The Benefits of Credential Evaluation

1. Enhanced Employability:

Credential evaluation helps U.S. employers understand your qualifications, making it easier for you to secure a job that matches your education and skills.

2. Educational Pursuits:

If you plan to continue your education in the United States, a course-by-course evaluation ensures that your prior coursework is recognized by U.S. institutions, potentially saving you time and money.

3. Professional Licensing:

Certain professions, like nursing or engineering, require specific educational backgrounds. Credential evaluation ensures your foreign education meets these requirements.

4. Immigration and Visa Applications:

When applying for immigration visas or employment-based visas, accurate credential evaluation is often a requirement to demonstrate your eligibility.

5. Accurate Placement:

Credential evaluation helps place you in appropriate academic programs or professional positions, ensuring you’re neither overqualified nor underqualified for your chosen path.

In conclusion, the process of evaluating foreign educational credentials is a crucial step for individuals looking to make the most of their international education in the United States. It bridges the gap between diverse educational systems, enabling employers, institutions, and licensing boards to understand and appreciate the value of your foreign qualifications.

A&M Logos International has been producing evaluations of foreign educational credentials for over 20 years. We always try to evaluate your documents to show the most advantageous result in terms of US degrees and credit hours. Call us today at (212) 233-7061 or e-mail us at info@apostille.us. You can also apply on our website.

A certificate of incorporation, also known as articles of incorporation or a corporate charter, is a legal document that is filed with the state government to create a corporation. It is the basic governing document of a corporation and contains information about the corporation’s name, purpose, location, and structure. A similar document, often called a Certificate of Formation, is filed to register an LLC or partnership.

It

is worth bearing in mind that some states will issue a certificate to

confirm the registration of a given company, while in others the same

purpose would be served by a certified copy of the articles of

incorporation filed with the state.

The

specific requirements for certificates of incorporation vary from

state to state. However, there are some common elements that are

typically included:

The

name of the corporation

The

purpose of the corporation

The

location of the corporation’s principal office

The

number of authorized shares of stock

The

names and addresses of the initial directors and officers of the

corporation

The

name and address of the corporation’s registered agent

In

addition to these common elements, some states may have additional

requirements. For example, some states require corporations to

include a statement of their intended duration (e.g., perpetual or

for a specified period of time) or a provision for amending their

articles of incorporation.

Here

are some examples of differences between states in terms of

certificate of incorporation requirements:

Delaware:

Delaware

is known as a “business-friendly” state and has relatively

few requirements for certificates of incorporation. For example,

Delaware does not require corporations to include a statement of

their intended duration or a provision for amending their articles

of incorporation.

California:

California

has more stringent requirements for certificates of incorporation

than Delaware. For example, California corporations must include a

statement of their intended duration and a provision for amending

their articles of incorporation.

New

York: New

York has requirements that are similar to California’s. However, New

York also requires corporations to include a statement of their

authorized capital stock. The

State requires new corporations to state how many shares they would

be issuing as well as if they have par value (below which the price

cannot drop).

When

choosing a state to incorporate in, it is important to consider the

specific requirements of that state. Here are some additional things

to keep in mind when filing a certificate of incorporation:

The

filing fee for a certificate of incorporation varies from state to

state.

The

certificate of incorporation must be signed by the incorporators of

the corporation.

The

certificate of incorporation must be filed with the secretary of

state of the state in which the corporation is being incorporated.

The

corporation will not be considered legally formed until the

certificate of incorporation is filed and approved by the secretary

of state.

If you need assistance filing your certificate or articles of incorporation / formation to set up a corporation, partnership, LLC, or other entity in the United States, feel free to contact us by calling us at (212) 233-7061 or e-mailing us at info@apostille.us. You may also wish to visit our website.

We

can also assist you with retrieving your certificate of incorporation

/ formation or a certified copy of your articles of incorporation /

formation and apostilling or legalizing them for use abroad.

If you are applying for a foreign visa, permanent residency, or citizenship, you may be required to provide a background check. The specific requirements for background checks vary from country to country, so it is important to check with the embassy or consulate of the country you are applying to for specific information.

In general, there are two types of background checks that are commonly required for foreign visas, permanent residency, or citizenship:

State-level criminal background checks: These checks search the criminal history database of the state where you reside or last resided.

FBI background checks: These checks search the FBI’s National Crime Information Center (NCIC) database, which includes records of arrests, convictions, and dispositions from all 50 states and the District of Columbia.

The specific requirements for background checks also vary depending on the purpose of your visa. For example, if you are applying for a student visa, you may only need to provide a state-level criminal background check. However, if you are applying for a work visa, you may need to provide an FBI background check. Again, the specific requirements vary from country to country and depend on the purpose of your application.

It is important to bear in mind that the FBI background check is based on your name, date of birth, and fingerprints. The application can be easily filed online on the website of the FBI. Once the application is submitted, the fingerprints can be either mailed in or submitted via a participating USPS office.

The FBI generally issues the background in about 2-3 weeks. However, in most cases, you would also need to get it apostilled or authenticated at the federal level, which currently takes up to 2-3 months. That is why it may a good idea to check if a state-level background check would be acceptable instead of a federal FBI check.

Unlike the FBI background check, state-level background checks are based solely on state police databases. Moreover, many states do not require fingerprints to issue background checks, as the searched is based on your name and date of birth. Some states offer both fingerprint-based and name-based background checks, so make sure to check with the destination immigration agency or consulate if such background checks would be acceptable.

Most countries will also require your background check to be duly legalized. If the country is an Apostille Convention member, you would need to obtain an apostille. An apostille is an official certification that a document is genuine. It is required by some countries as a way to verify the authenticity of a document.

If the country is not a member, the document would need to undergo chain legalization. For most countries, this means getting the document authenticated at both the state and federal levels (federal documents, such as FBI background checks, only need to be authenticated at the federal level) before getting it legalized with the respective country’s embassy or consulate. Some countries, such as Vietnam, only require state-level authentication. China, which is in the process of transitioning to becoming a member of the Apostille Convention, requires both state and federal authentication for documents issued in states within the Chinese embassy’s jurisdiction (generally encompassing the South and Mountain States), but only state-level authentication is required if the document originates from the jurisdiction of any of the other Chinese consulates (New York City, Chicago, Los Angeles, or San Francisco). If you are not sure what to do, feel free to contact us, and one of our specialists will be more than happy to assist you.

The process of getting a background check for a foreign visa, permanent residency, or citizenship can be time-consuming and expensive. However, it is important to comply with the requirements of the country you are applying to in order to avoid delays or denial of your visa application.

Here are some additional tips for getting a background check for a foreign visa:

Start the process early. It can take several weeks to get a background check, so it is important to start the process early.

Check with the embassy or consulate of the country you are applying to for specific requirements.

Be prepared to pay the required fees.

Make sure that your background check is apostilled, if required.

A&M Logos International has over 30 years of experience dealing criminal background checks for use abroad. Call us today at (212) 233-7061 or e-mail us at info@apostille.us. You may also wish to apply through our website.

Going through a divorce can be a difficult and emotional process. There are many legal and financial details to consider, and it can be easy to get lost in the paperwork. Two important documents that are often confused are divorce certificates and decrees.

What

is a divorce certificate?

A

divorce certificate is a legal document, typically

issued by the state, to

confirm that a marriage has been legally dissolved. It typically

includes the names of the former spouses, the date of the divorce,

and the location of the divorce. Divorce certificates are often

required for government-related purposes, such as changing your name

or remarrying.

What

is a divorce decree?

A

divorce decree is a court order that finalizes a divorce. It is a

more detailed document than a divorce certificate, and it typically

includes information about the following:

The

division of property and debts

Child

custody and visitation

Spousal

support (alimony)

Other

terms agreed to by the spouses

Divorce

decrees are not always required by the government, but they can be

helpful in resolving disputes between former spouses. They can also

be used to enforce the terms of the divorce, such as child support

payments.

The

problem is somewhat compounded by the fact that some jurisdictions in

the United States do not issue divorce certificates. For example, the

State of California does not issue divorce certificates for divorces

that occurred after 1984. In such cases, the only document that can

serve as confirmation of the divorce would be a certified or

exemplified copy of the divorce decree from the court in which the

couple had gotten divorced.

Both

divorce certificates and decrees can be apostilled or authenticated,

although one would generally need to retrieve a certified or

exemplified copy of the divorce decree containing the signature of

the clerk of the court in order for the state to apostille or

authenticate the decree. If a state issues divorce certificates, one

would generally need to apply for it with the state’s vital records

agency and then get that certificate apostilled or authenticated.

Some

foreign officials do not always understand the fact that the United

States has a very decentralized vital records system, with many

records often only available at the state or local level. Moreover,

many fail to understand the fact that divorce certificates are not

available in many US states, with the certified or exemplified copy

of the divorce decree having the same effect as a certificate in such

jurisdictions. This can create problems for US citizens seeking to

get married or apply for certain visa categories in foreign

countries.

A&M Logos International has been retrieving, processing, and legalizing divorce decrees and certificates for more than 30 years. If you need assistance retrieving and legalizing your decree or certificate for use abroad, call us at (212) 233-7061 or e-mail us at info@apostille.us. You may also wish to apply on our website.

It may come as a surprise that US state and local law varies considerably regarding availability of marriage certificates to the general public. One can differentiate the following types of marriage records:

Public

records: In

some

states,

marriage records are public records. This means that anyone can

request and obtain a copy of them, for any reason. There are no

restrictions on who can access public marriage records.

Confidential

records: In

other

states,

marriage records are confidential. This means that only the parties

involved, their relatives, or their legal representatives can access

them. There are a few reasons why a marriage record might be

confidential, such as if the couple is under the age of 18, if the

marriage is annulled, or if the couple is seeking a divorce.

Restricted

records: In

some states, marriage records are restricted. This means that they

are only accessible to certain people, such as government officials,

researchers, or journalists. There are a few reasons why a marriage

record might be restricted, such as if it contains sensitive

information about the parties involved.

It

is important to note that the laws regarding access to marriage

records can vary from state to state. If you are unsure about the

laws in your state, you can contact us to go over the law in your

state.

As

an example, here is an overview of the law in some states:

In

California, informational marriage records are unrestricted, but

certified authorized copies can only be obtained by the individual

whose name appears on the certificate, their parents, their

guardians, their descendants, an attorney, attorney-in-fact, or a

member of a law enforcement agency. Confidential records can only be

requested by the individual whose name is on the certificate.

In

New York, marriage records are confidential for the first 50 years

after the date of marriage. This means that only the parties

involved, their relatives, or their legal representatives can access

them during this time period. After 50 years, marriage records

become public records.

In

Florida, marriage records are available to anybody without the need

for a power of attorney or notarized authorization letter.

The

laws regarding access to marriage records can have a significant

impact on people’s lives. For example, if a person is trying to prove

that they are married for immigration purposes, they may need to

obtain a copy of their marriage record. If the marriage record is

confidential or restricted, this may make it difficult or impossible

for the person to obtain the documentation they need.

It is important to be aware of the laws regarding access to marriage records in your state. If you intend to use your marriage certificate in a foreign country, you will need to make sure that the type of record would be eligible to get legalized. Call us today at (212) 233-7061 or e-mail us at info@apostille.us to discuss how we could go about retrieving and obtaining an apostille for (or legalizing) your marriage certificate. You can also submit your application on our website (https://apostille.us/Documents/Document_Marriage_Certificate.shtml. Our experienced team of experts will go over your particular situation and figure out a way to retrieve your records as quickly and as effortlessly as possible.

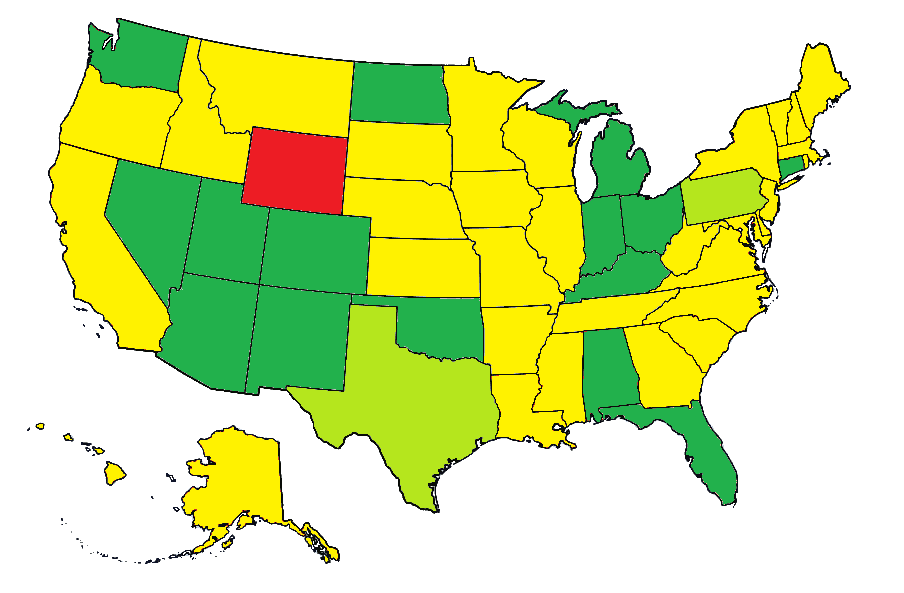

Provided below is a map for your reference state law differences on the availability of marriage records to the general public. States in GREEN have public marriage records. States in LIGHT GREEN have varying local law regarding the availability of marriage records (fully public in some counties and available to unrelated individuals with a notarized power of attorney or authorization letter). States in YELLOW release marriage records to unrelated individuals with a notarized power of attorney or authorization letter. Finally, the sole state in RED (Wyoming) only releases marriage records to the individual whose name appears in the certificate or a licensed attorney.