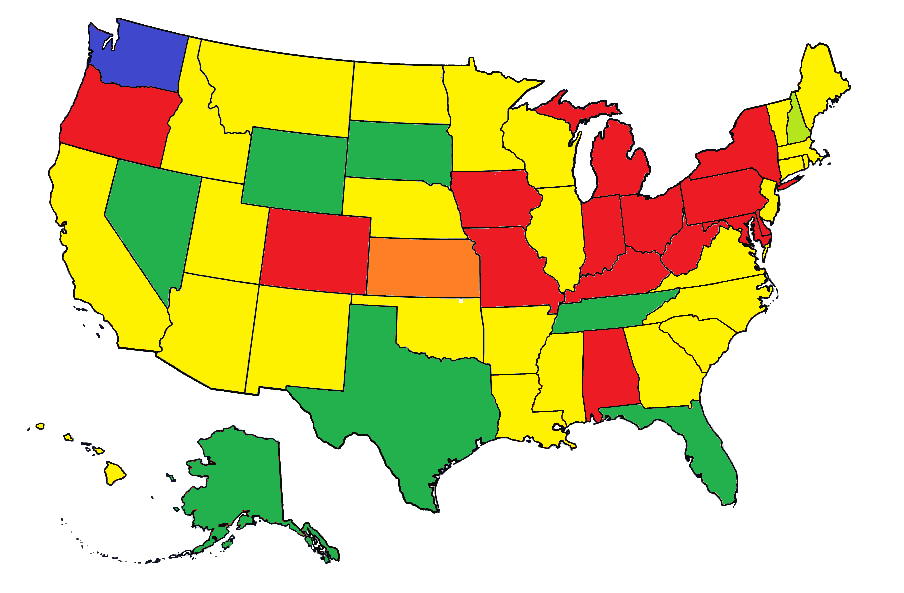

Light green: States with income tax on interest and dividends only (currently only New Hampshire)

Blue: States with income tax on certain long-term capital gains only (currently only Washington)

Yellow: States with state income tax, but no local income taxes

Orange: States with state income tax and local income taxes on interests and dividends only (currently only Kansas)

Red: States with state and local income taxes

Tax residency is a concept that lies at the core of an individual’s tax obligations. For most people, it’s relatively straightforward: you reside in a particular place, and that place’s tax laws apply to your income. However, the nuances of tax residency become considerably more complex when you factor in multiple states and the influence of mutual tax treaties. Each state in the United States has its own rules for determining tax residency, and these rules can significantly impact an individual’s tax liability. This article explores the intricacies of state-level tax residency rules, mutual tax treaties, and the challenges individuals face when dealing with multi-state taxation.

State-Level Tax Residency Rules

Each state has its own set of rules for determining tax residency. While there are some commonalities, such as the general notion that residency is based on where you live, important differences exist. Here are some key factors that states often consider:

1. Domicile vs. Statutory Residency: Many states distinguish between domicile (where you intend to make your permanent home) and statutory residency (where you spend a significant portion of the year). Some states may consider you a resident if you maintain a domicile within their borders, even if you spend most of your time elsewhere.

2. Physical Presence: The number of days you spend within a state’s borders is a common factor in residency determinations. States may have different thresholds, such as 183 days or more in a tax year.

3. Home Ownership or Rental: Owning or renting a home in a state can be a factor. Owning property in a state may suggest a stronger connection to that state.

4. Family and Business Ties: Having close family members or a business in a state can also influence your residency status.

5. Voting and Driver’s License: Registering to vote or obtaining a driver’s license in a state can be viewed as evidence of residency.

Mutual Tax Treaties and State Residency

Muutal tax treaties between states can further complicate the issue of tax residency. These treaties are agreements between states that aim to prevent double taxation and clarify residency rules for individuals with ties to multiple states. They often provide criteria for determining residency in cases of conflict between states.

However, it’s essential to note that not all states have mutual tax treaties with each other, and the provisions of these treaties can vary widely. Therefore, individuals navigating multi-state taxation should be aware of the specific treaties that apply to their situation and how they may impact their tax liability.

Mutual tax treaties play an important role in the case of individuals who work in one state but reside in another.

For example, since New York does not have any mutual tax treaties governing reciprocity with any other states, individuals who work in New York, but live in, for example New Jersey or Connecticut, must still file a New York state non-resident income tax return (Form IT-203) and then also file their state-s resident income tax return (Form NJ-1040 in the case of New Jersey or Form CT-1040 in the case of Connecticut), taking a tax credit for the taxes already paid to New York.

On the other hand, New Jersey has a mutual tax treaty governing reciprocity with Pennsylvania. Individuals who live in Camden, New Jersey, but commute to Philadelphia, Pennsylvania, for work, do not need to file a Pennsylvania personal income tax return (Form PA-40), but must file a New Jersey tax return to report their income and pay the entirety of the taxes owed. Pennsylvania employers would be required to withhold New Jersey income tax for employees that reside in New Jersey. That being said, the situation is further complicated by the fact Pennsylvanian municipalities and school districts do not adhere to the mutual tax treaty, so if we take the aforementioned example, Philadelphia non-resident wage tax would still be withheld (a tax credit for the tax withheld locally can also be claimed on the New Jersey income tax return). While Philadelphia does not require individuals to file a tax return if their employer fully withheld the tax, low income taxpayers may benefit from filing a wage tax refund petition with the city.

A resident of Philadelphia working in Camden would also not need to file a New Jersey income tax return, but the income received in New Jersey would need to be reported on their Pennsylvania income tax return. Also, unless their New Jersey employer voluntarily withholds Philadelphia Wage Tax, they would need to register to file and pay earnings tax with the city. If the individual resides anywhere else in the Commonwealth of Pennsylvania, they will likely be required to pay quarterly taxes to their local earned income tax collector (collecting taxes for municipalities and school districts).

By virtue of its status, the District of Columbia does not tax non-residents, so individuals who live in Maryland or Virginia, but commute to DC for work only need to file and pay taxes in their respective states of residence. On the other hand, DC residents who work in Maryland and Virginia only need to file and pay taxes in Washington, DC.

There are also some states that have unilateral tax treaties governing reciprocity. For example, residents of California working in Arizona do not need to file and pay Arizona taxes, but must report their entire income on their California resident income tax return. Their Arizona employers would need to withhold California taxes from their salary. On the other hand, an Arizona resident working in California would be required to file and pay California income tax. Their California employers would only need to withhold California taxes from their pay. Once they file their California taxes, they would also need to file an Arizona resident income tax return, taking a tax credit for the California taxes already paid.

Proving Non-Residency and Challenges

Proving that you are no longer a resident of a particular state can be a complex and challenging process. Some states may require documentation such as lease agreements, utility bills, or sworn affidavits to demonstrate your intent to change your domicile. However, mere declarations may not always suffice, especially if you maintain ties to the state, such as a vacation home or continued business interests.

Additionally, situations where individuals live in one state and work in another can be particularly tricky. The general rule of thumb is that states tax based on both residency and source of income, although the aforementioned tax treaties outline situations in which individuals only need to pay taxes to the state in which they reside. Some localities also tax both residents and individuals sourcing income from that jurisdictions, while others tax only residents or only individuals/businesses sourcing income from the jurisdiction. Navigating the intricacies of these rules and ensuring compliance can be a daunting task.