When it comes to filing taxes in the United States, we usually hear about federal income taxes and state income taxes, but we rarely hear about local income taxes. Compounding the problem is the fact that most tax preparation software and even some professional accountants rarely focus on local income taxes, which may lead to unexpected tax surprises, or, even worse, penalties and interest years later. Adding to the complexity is the fact that different localities use different tax bases, with some only taxing earned income, and others only taxing interest and dividends as well as the fact that in some states, local income taxes are reported on state income tax returns, while in others they must be filed separately.

For your convenience, we have broken down this article by states that allow local income taxes. The states are not in geographical, rather than alphabetical order, going from east to west. Note that the purpose of the articles is purely informational and should not be taken as tax advice. A&M Logos International assumes no responsibility for the accuracy of the information provided.

If you have questions about filing local income taxes or need assistance with preparing federal, state, or local income tax forms or obtaining US tax residency certification, please contact us at (212) 233-7061 or e-mail us at info@apostille.us. You may also wish to visit our website.

- New York

- Pennsylvania

- Delaware

- Maryland

- Virginia

- Alabama

- Kentucky

- West Virginia

- Ohio

- Michigan

- Indiana

- Iowa

- Missouri

- Kansas

- Colorado

- New Mexico

- California

- Oregon

- Washington

- Hawaii

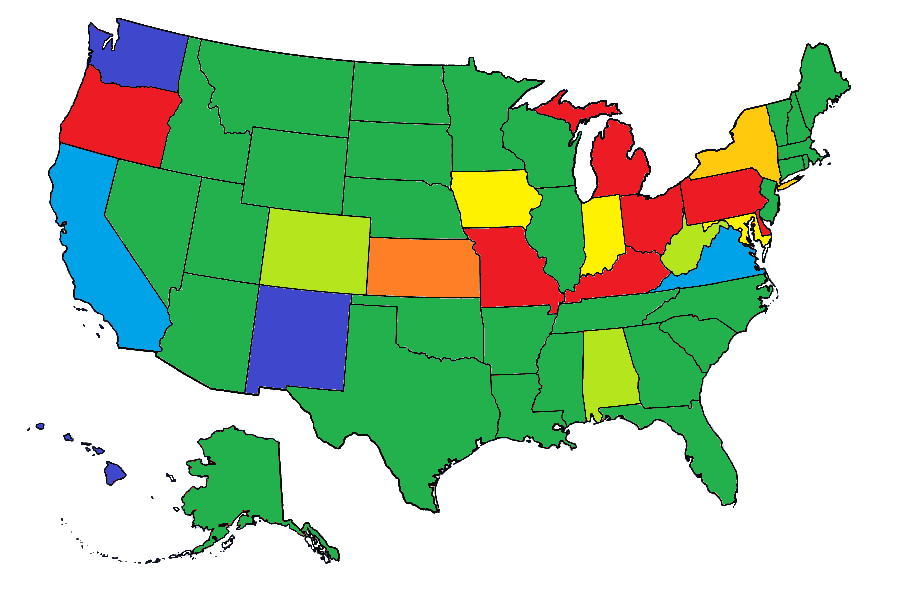

Green: No local income taxes

Light Green: Local income taxes withheld by employer usually with no individual filing requirement

Yellow: Local income taxes included on standard income tax form

Gold: Local income taxes included on standard income form, with separate filing with city for self-employment income over a certain threshold as well as nonresident wage earners (currently only New York)

Orange: Local income taxes on interest and dividend income only (currently only Kansas)

Light Blue: Local business income taxes for self-employed individuals

Dark Blue: State and local business taxes

Red: Local income taxes must be filed separately with locality or local income tax collector (some jurisdictions require filing only if local income tax is not fully withheld by employer; others have mandatory filing for all residents)

New York: The Empire State of Local Income Taxes

The State of New York has 3 different local income taxes—New York City income tax, Yonkers income tax, and the Metropolitan Commuter Transportation Mobility Tax. All 3 taxes are collected on the standard state income tax form (IT-201 for residents or IT-203 for non-residents and part-year residents). If you changed your New York City or Yonkers residence status, you would also need to file Form 360.1.

New York City only imposes an income tax on individuals who are residents of New York City. If you do not live in New York City but earn income within the city, you are not subject to the New York City income tax, unless you are employed by New York City (in which case you would have section 1127 income withheld from your paycheck and would need file Form 1127 with New York City).

Yonkers, on the other hand, subjects both residents and non-residents to the city’s income tax. If you are a resident of Yonkers, you can calculate Yonkers income tax on the New York State income tax return. If you are a non-resident with Yonkers-sourced income, you would also need to file Form Y-203 with your New York State income tax return.

It is worth noting that New York City uses a wide income tax basis for taxable income, including both earned and unearned income. Yonkers residents are subject to a surcharge on the income tax paid to New York State, while non-residents are only taxed on wages and self-employment income earned in Yonkers.

Finally, the Metropolitan Commuter Transportation Mobility Tax is only imposed on self-employment income in excess of $50,000 sourced from New York City, as well as Nassau, Suffolk, Westchester, Rockland, Putnam, Dutchess, and Orange counties. It is also a payroll tax payable by employers operating within that area (the Metropolitan Commuter Transportation Mobility District) and is used to finance the Metropolitan Transit Authority (MTA).

It is also worth noting that self-employed individuals and unincorporated businesses sourcing income from New York City may also be required to file New York City Form 202, New York City Unincorporated Business Tax return, if their self-employment income exceeds $95,000.

Pennsylvania: Many Local Taxes, One Commonwealth

The vast majority of Pennsylvania cities and school districts impose a local income tax. It is important to note that all localities except the City of Philadelphia are governed by Pennsylvania Act 32.

Act 32 municipalities and school districts are allowed to levy a Local Earned Income Tax. It is important to bear in mind that Local Earned Income Tax is included on the Pennsylvania State income tax return (Form PA-40), but must be filed with the local earned income tax collector. A local earned income tax collector is a private company authorized by a given county to collect local earned income taxes for municipalities and school districts within that county. Each county except Allegheny County has one tax collector for the entire county. Allegheny County (which includes the City of Pittsburgh) is split into 4 tax collection districts and currently uses 2 tax collectors (Jordan Tax Service and Keystone Collections Group).

To determine which tax collector collects taxes for your locality, you may wish to use an address lookup tool provided by the Pennsylvania Department of Community & Economic Development. It is crucial to remember to file your local earned income tax return with your local earned income tax collector as failure to do so will result penalties and interest years down the line. Pennsylvania employers must generally withhold local earned income tax based the higher rate of where you live or work, but you must still file at the end of the year to avoid getting penalized for failure to file. Since the tax is always a flat rate (PA law essentially prohibits progressive or regressive taxation), there would generally be no additional tax liability or refund if your employer fully withheld the tax due. If your employer does not withhold local earned income tax, you must make sure to file those tax remittances with the local earned income tax collector on a quarterly basis.

Bear in mind that Pennsylvania employers must also withhold another local taxed known as a Local Services Tax. The Local Services Tax is a flat annual fee, which is generally limited to $52 per year (with the exception of “financially distressed municipalities” which can collect more). The Local Services Tax is generally collected by splitting the annual fee into payroll periods and then withholding the tax from each paycheck (e.g. if payroll is done a weekly basis, a $52 will be split into 52 equal payments of $1 collected from each weekly paycheck until the end of the year). Individuals can apply for a refund of their Local Services Tax collected if their total earned income is below a certain limit (generally $12,000). Note that unlike the local earned income tax, local services tax are always paid to the municipality in which an individual does their work (rather than resides), although residence can be a factor in the cases of multiple employers. The local earned income tax collector often also collects local services tax for the same jurisdiction, but that is not always the case.

Pennsylvania is also unique in that some municipalities also impose a flat-fee occupational tax based on the locality’s assumption of the income you would be making from your job, and per capita tax, levied for the privilege of remaining alive withing a given locality. Note that individuals with low income can generally apply for an exemption from these taxes. Collection of these taxes is sometimes, but not necessarily handled by local earned income tax collectors.

The aforementioned taxes do not apply to the City of Philadelphia, which administers its own income tax system. Wage earners working in Philadelphia generally have Philadelphia Wage Tax withheld from their paycheck. If the employer fully withheld Philadelphia Wage Tax, there is no filing requirement at the end of the year, unless the taxpayer wants to apply for a refund (generally applicable if the individual receives less than the federal poverty level).

Philadelphia residents who did not have Philadelphia Wage Tax withheld from their wages must register an account to pay Philadelphia Earnings Tax on a quarterly basis. At the end of the year, you would need to file an Annual Reconciliation of Employee Earnings Tax return with the City of Philadelphia.

Philadelphia also taxes certain unearned income such as interest, dividends, and rental income, and capital gains, so if you have those items of income, you would be required to file a Philadelphia School Income Tax return.

Finally, if you are a Philadelphia resident with self-employment income (from any source) or have Philadelphia-sourced self-employment income, you would need to register as a business and file a Net Profits Tax return with the City of Philadelphia. Gross receipts (i.e. income without any deductions) from Philadelphia-sourced self-employment are also subject to the Philadelphia Business Income & Receipts Tax. If your income is below the threshold, you would still need to file a “No Tax Liability” tax exemption form. It is important to underscore that Philadelphia Net Profits Tax (NPT) and Business Income & Receipts Tax (BIRT) are 2 separate taxes on self-employment income, although a partial credit can be applied to NPT for BIRT previously paid.

Delaware: The First State and the Lone Local Tax

The only locality to have an income tax in the State of Delaware is the City of Wilmington. If you are employed by a Delaware employer and are a resident of Wilmington or you are a non-resident of Wilmington but work in the city, your employer would be required to withhold Wilmington Earned Income Tax, in which case you would not need to file any return at the end of the year. If, however, you are a Wilmington resident and your employer does not withhold Wilmington Earned Income Tax (as could be the case if you live in Wilmington but work out of state), you would need to set up a self-reporting employee earned income taxpayer account and file and pay Earned Income Tax with the City of Wilmington on a quarterly basis.

If you are a resident of Wilmington with self-employment or rental income (as well as certain business-related capital gains) or you have those items of income sourced from Wilmington, you would need to file a Wilmington Net Profits Tax return to pay Wilmington Net Profits Tax.

Maryland: A County-by-County Tale

All counties of Maryland as well as the City of Baltimore impose a Local Income Tax on the same items of income as the State of Maryland. Local Income Tax in Maryland is levied by the county (or independent city) in which you reside. It is calculated and reported on the Maryland resident income tax return (Form 502).

If you are not a resident of Maryland, you would generally not be liable for local income taxes, which is why local income tax is not included on the Maryland non-resident income tax return (Form 505). However, if you are a resident of a local jurisdiction in New York, Pennsylvania, Delaware, Alabama, Kentucky, Ohio, Michigan, Indiana, and Missouri that imposes an income or earnings tax on residents of Maryland, you must file Maryland Form 515 to calculate your Maryland local income tax liability.

Virginia: A Commonwealth of Local Business Taxes

The Commonwealth of Viginia does not have local income taxes per se, but self-employed individuals may be required to register with the county or independent city from which they derive their self-employment income. Many counties and independent cities exclude gross receipts below $10,000 from local Business License Tax. Note that some counties and independent cities may also require the filing of a personal business property tax return.

While you may think you can get away with not registering your self-employment activities, you may wish to consider the fact that the Virginia Department of Taxation provides information on individuals who filed Federal Schedule C to independent cities and counties. This informational exchange is pretty new and will often not be of concern to those who received less than $10,000 in gross receipts. However, it is always a good idea to check registration requirements and fees with your independent city or county.

Alabama: A Local Twist

A number of cities in Alabama require employers to withhold a Local Occupational Tax (a flat percentage tax) from each paycheck paid to employees. The tax is paid on income sourced from the municipality imposing the tax. This tax is generally not refundable and there is no obligation on the part of individuals to file this tax (unless they are employers).

Kentucky: Local Taxes Galore

Most counties and municipalities, as well as some school districts (usually sharing boundaries with their respective counties), impose local income taxes on income earned withing that particular jurisdiction. For school districts, the rate varies depending on whether the individual earning the income is a resident of that school district or not. For counties and municipalities, on the other hand, the rate generally does not vary based on residence status.

Employers are required to withhold the local income tax, often known as Occupational License Tax or Occupational Tax from the paychecks of their employees. Employees are generally not required to file any tax returns at the end of the year.

At the same time, if you had self-employment income or certain rental income sourced from a given Kentucky county, school district, or municipality, you would generally need to register with that jurisdiction to file and pay the income tax, which in these scenarios is often referred to as the Net Profits Tax (but sometimes the same name—Occupational License Tax or simply Occupational Tax—may be used in reference to self-employment). In some cases, like the consolidated Louisville/Jefferson County Metro or Lexington-Fayette Urban County, it is sufficient to file 1 return. In other cases, 2 or even 3 different returns may need to be filed. For example, an individual with self-employment income from Bowling Green, would need to register and file 3 separate Net Profits Tax returns with Warren County, the Warren County Public School District, and the City of Bowling Green.

It is worth bearing in mind that as a W-2 salaried employee, you should generally not be worried about any local income tax filings in Kentucky. However, if you are self-employed, you should be aware that many Kentucky cities, counties, and school districts require payers of non-employee income to report those payees. Payees that fail to register and file with the respective county, school district, and/or municipality will be subject to penalties and interest on their unpaid occupational license / net profits tax.

West Virginia: City Services Fee

Some West Virginia municipalities require employers to withhold a flat City Services Fee from paychecks of employees. The tax is a flat fee deducted from employee paychecks on a weekly basis (e. g. $3 per week as is the case for Charleston). Employees with multiple employers should make sure to inform their new employer that their first employer is already withholding the City Services Fee to avoid having the fee withheld twice. In some cities, employees may also qualify for a refund of the fee if they get charged the same tax more than once by multiple employers. No end-of-year tax return filing is required.

Ohio: Municipal and School District Income Taxes

Most municipalities in Ohio impose a Municipal Income Tax on income earned in that municipality as well as on any income earned by residents of that municipality. Local employers must generally withhold local income tax from the salaries of resident and non-resident employees. Generally, only earned and certain rental income is subject to local income tax.

Many Ohio municipalities, such as Columbus, Cincinnati, and Toledo, collect their income taxes directly. Some municipalities (e.g. Columbus, Cincinnati) only require individuals to file if their income tax was not fully withheld by their employer. Others impose a filing requirement on anybody with earned income or on any adult resident independent of income.

A number of Ohio municipalities do not collect their income tax directly but use the services of 1 of 2 tax collection agencies—the Regional Income Tax Agency (RITA) or the Central Collection Agency (CCA). RITA generally collects for some small to mid-sized municipalities spread out throughout Ohio, while CCA primarily collects for municipalities in the Cleveland metropolitan area, including Cleveland itself.

In addition to municipal income taxes, Ohio also allows school districts to levy an income tax. Ohio School District Income Tax is collected by the state, but it is not included on the standard state income tax return (Form IT 1040). A separate form, SD 100, must be filed with the State of Ohio if you are subject to the tax. It is worth bearing in mind that only some school districts impose the tax, so many Ohio residents do not have to worry about filing Ohio Form SD 100. School districts can pick whether to use a traditional tax base (generally all items of income taxed by the State of Ohio) or an earned income tax base. It is also worth remembering that School District Income Tax is only imposed on residents of that school district.

Michigan: City Income Tax

A number of Michigan cities impose a City Income Tax on both residents and non-residents with income sourced from that city (the rate for residents is usually higher). The income tax base is generally quite wide, so any income taxable by the State of Michigan would usually be taxable by a city imposing the income tax as well.

City income taxes are generally collected by the individual cities themselves. Individuals residing in those cities or having income sourced from those cities must generally file a city tax return if their income exceeds a certain threshold. The only city that does not collect its own income tax is Detroit, whose income tax is collected by the State of Michigan. It is not, however, reported on the standard Michigan income tax return (Form MI-1040), but on the State-issued Detroit Resident Income Tax return (Form 5118) or Detroit Non-Resident Income Tax return (Form 5119).

Indiana: County-Level Tax

All Indiana counties have a Local Income Tax imposed on both residents and non-residents with income sourced from that county. The county income tax is reported on the standard Indiana state income tax return, Form IT-40 for residents or Form IT-40PNR for non-residents and part-year residents.

Iowa: School and Emergency Medical Services Surtax

Many Iowa school district impose a School District Surtax on tax due to the State of Iowa on residents of that school district. In addition, Iowa allows counties to impose an Emergency Medical Services (EMS) Surtax. Appanoose County is currently the only county imposing the county surtax. These surtaxes are calculated on the standard Iowa State Income Tax return (Form IA 1040).

Missouri: Show Me the Earnings Taxes!

Missouri law allows the 2 largest cities of the state to impose local income taxes—St. Louis and Kansas City. In both cities, the tax can only be imposed on earned income and is known as the Earnings Tax. Residents of St. Louis and Kansas City are subject to the tax on income earned anywhere, while non-residents must only pay the Earnings Tax on income earned in St. Louis or Kansas City.

Taxpayers are not required to file any tax returns with their cities if their employer fully withholds the Earnings Tax (currently at 1% in both cities). If Earnings Tax is not fully withheld, as is often the case with individuals residing in St. Louis or Kansas City but working out of state, those individuals must file an Earnings Tax return with their respective cities. In St. Louis, that form is known as Form E-1, while in Kansas City it is called Form RD-109.

Kansas: Only Intangibles Taxed Locally in Sunflower State

The Sunflower State allows counties and municipalities to impose a local income tax on interest and dividends only. This is known as the Kansas Local Intangibles Tax. The tax is generally imposed on residents of a particular municipality or county if that locality imposes a local intangibles tax and the individual in question receives interest or dividend income. In certain cases, if the interest and/or dividend income is derived from property or business located in a locality imposing the tax, non-residents would also need to file and pay the tax.

Individuals owing Local Intangibles Tax in excess of $5 must file and pay the Local Intangibles Tax on State Form 200. Note that even though the form is issued by the state, it must the filed with the county tax collector where the tax is owed.

Colorado: Occupational Privilege Taxes in the Centennial State

Colorado allows municipalities to impose a flat-fee Occupational Privilege Tax, which is withheld by an employer from an employee’s paycheck. The Occupational Privilege Tax applies only to earnings made in the municipality imposing the tax and is not based on residence.

An employee would generally need to certain minimum amount to be subject to the Occupational Privilege Tax. For example, the City of Denver imposes an Occupational Privilege Tax of $5.75 per month payable by an employee (a corresponding $4 per month must be paid by the employer for each employee). The Denver Occupational Privilege Tax only applies if the employee received compensation of at least $500 in that month.

While most municipalities imposing the Occupational Privilege Tax provide for a minimum monthly income that must be met for the tax to be imposed, this is not always the case. For example, the City of Sheridan imposes a $3 per month Occupational Privilege Tax on any employee working in the city (with a corresponding employer payment of $3).

Individuals are generally not required to file any returns, but employees should be cognizant of the tax in the case of having multiple employers, as new employers may not be aware that the required tax is already being withheld.

New Mexico: Self-Employed Beware of the Gross Receipts Tax!

New Mexico does not have local income taxes per se, but most self-employed individuals are required to register for and file the New Mexico Gross Receipts Tax, which is often equated with a sales tax, as it can be passed on to the final consumer (although final liability for its payment lies with the business or self-employed individual). Note that unlike sales taxes in other states, most services are subject to New Mexico Gross Receipts Tax. And because of a tax information exchange program between the IRS and New Mexico, the State will find out that you filed a Schedule C sooner or later and, like it or not, send you a penalty notice if you have not registered and filed the appropriate forms.

The local component of the Gross Receipts Tax is calculated when filing Form TRD-41413 (the New Mexico Gross Receipts Tax return) with the State. Individuals are required to register by filing Form ACD-31015 with the State of New Mexico when they start engaging in or deriving income from self-employment.

California: Business Tax Traps for the Self-Employed working in the Municipalities of the Golden State

California does not impose any local income taxes per se, but many municipalities require self-employed individuals to obtain a Municipal Business Tax Certificate, or Business License, which generally requires payment of a business license fee or business tax. Some counties may also have a business tax or license requirement, especially for those in unincorporated areas of the counties.

In some municipalities, individuals with gross receipts or earnings below a certain threshold can apply for an exemption (e. g. in the City of Los Angeles, the “small business exemption” exempts self-employed individuals with gross receipts under $100,000 from paying the business tax, but those individuals must apply for an exemption on time).

Note that that the deadline to pay business license fees or to apply for an exemption is often earlier than the regular tax filing deadline. Self-employed individuals must generally register when they start engaging in business, however. Also, bear in mind that California municipalities and counties can easily find out if you have filed a Schedule C because of a tax information program with the California Franchise Tax Board.

Oregon: A Wild Mishmash of Local Taxes in the Beaver State

While the State of Oregon is one of the few states that does not have a sales tax at either the state or local level, Oregon has a multitude of crisscrossing and overlapping local income taxes, particularly in the Portland and Eugene metro areas.

First of all, in addition to Oregon State Income Tax, residents of Oregon and non-residents of Oregon working in the state are subject to the Oregon Statewide Transit Tax aimed at funding public transit services in the state. Residents of Oregon who work for an out-of-state employer who does not withhold that tax must pay the 0.1% tax by filing Oregon State Form OR-STI.

All individuals aged 18 or older who live in the City of Portland are subject to a $35 per person flat-fee Arts Tax aimed at financing arts education in the city. These individuals must file an Arts Income Tax return with the City of Portland. Individuals who earn less than $1,000 per year or are part of a household making less than the federal poverty level are exempt from paying the $35 Arts Tax, but must still qualify for the exemption by filing the Arts Income Tax return with the city.

The City of Portland also collects 2 local personal income taxes, both of which to single or married filing separately individuals earning over $125,000 per year (the threshold is increased to $200,000 a year for married filing jointly households as well as heads of household or qualifying surviving spouses). The income base for both taxes is wide, coinciding with Oregon’s definition of taxable income and includes both taxable and non-taxable income.

The first local income tax is known as the Metro Supportive Housing Services (SHS) Personal Income Tax and is a 1% tax applicable to income made over the filing threshold by residents of the area within the jurisdiction of the Portland Metro, a regional government (the only regional government in the United States) that encompasses the City of Portland as well as other areas of Multnomah, Clackamas, and Washington counties outside of Portland (but not the entire counties). The tax also applies to non-residents having income sourced from the Portland Metro in excess of the threshold. Metro Residents with income in excess of the filing threshold must file Portland Form MET-40, while non-residents with Metro-sourced income in excess of the threshold must file Portland Form MET-40-NP. The forms must be filed with the City of Portland. The tax is used to finance shelters and other housing services for individuals facing homelessness.

The second local tax is known as the Multnomah County Preschool For All (PFA) personal income tax and is a 1.5% tax applicable to income made over the filing threshold by residents of the entirety of Multnomah County. The tax also applies to non-residents having income sourced from Multnomah County in excess of the threshold. Multnomah County residents with income in excess of the threshold must file Portland Form MC-40, while non-residents with income sourced from Multnomah County above the threshold must file Portland Form MC-40-NP. As with the Metro SHS tax, both form are filed with the City of Portland.

The City of Portland provides an option to file a combined Metro SHS and Multnomah County PFA tax return online.

Individuals who are self-employed face an additional layer of complexity with regard to local income taxes in Oregon.

First of all, self-employed individuals making over $400 a year in the Tri-County Metropolitan (TriMet) Transportation District (the public transit district that services the Portland metropolitan area covering Multnomah, Clackamas, and Washington counties) or the Lane County Mass Transit District (the public transit district that services the Eugene metropolitan area covering Lane County) must file and pay an additional self-employment transit tax. Note that the boundaries of the districts do not necessarily coincide with the boundaries of the counties they service and are subject to change.

TriMet Transportation District Self-Employment Tax must be reported on Oregon State Form OR-TM, while Lane County Mass Transportation District Self-Employment Tax must be reported on Oregon State Form OR-LTD. Both forms are filed with the State of Oregon.

If your self-employment income is derived from the City of Portland and/or Multnomah County, you would also be subject to the City of Portland Business License Tax and/or Multnomah County Business Income Tax. Both the City of Portland and Multnomah County provide exemptions for gross income from all sources below a certain threshold ($50,000 for Portland and $100,000 for Multnomah County). Both taxes must be filed on Portland Form SP (Combined Tax Return for Individuals) with the City of Portland. In order to file the form, a self-employed individual would first need to register as a business with the City of Portland.

Self-employed individuals with income in excess of $5,000,000 derived from Portland Metro must also pay an additional 1% Metro SHS Business Income Tax. It appears that the tax can currently only be paid online, although it appears that the City of Portland may also issues a standalone Metro SHS Business Income Tax form in the future.

Finally, individuals with self-employment income in excess of $400 per year sourced from the City of Eugene must file and pay the City of Eugene Self-Employment Tax. The tax is a counterpart to the Eugene Community Safety Payroll tax aimed at financing local law enforcement. The tax is filed of City of Eugene Form EUG-SE. Individuals must first register as a business via the online MuniREVS resource to be able to file the tax return.

Washington: No Income Tax, but the Self-Employed must beware the B&O Tax

The State of Washington has no local (or state) income tax per se (although a state-level capital gains tax on certain long-term capital gains was implemented in 2021). However, individuals who are self-employed must be aware of the Washington Business & Occupation (B&O) Tax, which is imposed on gross income (i. e. your income without the deduction of any expenses, such as labor, materials, taxes, or fees) sourced from the State of Washington. The tax rate varies depending on the exact type of business. If you are self-employed, your business will likely fall under the services category, which has a rate of 1.5% of gross income (increased to 1.75% if the previous year’s gross income attributable to the activity was $1,000,000).

Note that you are not required to register with the State of Washington if your Washington-sourced self-employment gross income is under $12,000. It is therefore vital to monitor your revenue throughout the tax year. As soon as you hit the $12,000 mark, you would need to file a Business License Application (Form 700 028) with the State and pay the registration fee (currently $50).

If your self-employment is carried on within the boundaries of a particular Washington municipality, that municipality may also require you to obtain that municipality’s business license and pay the registration fee. The State of Washington provides a City and County Addendum (Form 700 060) to their state Business License Application for many (but not all) Washington municipalities.

Some municipalities, most notably Seattle, have a separate process for business registration. If you register with the state, it is also a good idea to register with the municipality in which you conduct your self-employment.

If you conduct your self-employment activities in an unincorporated area of a given Washington county, you may need to register and pay the business license fee with the county. The State of Washington collects the fee only for Asotin and Franklin Counties (currently $25 and $150, respectively). Many, but not all, counties do not require self-employed individuals to register or pay a business license fee.

If you register with the State, you would generally be required to file a Combined Excise Tax on annual, quarterly, or monthly basis (depending on your total gross income). The return is used to calculate and pay the B&O Tax owed.

If you registered with a municipality, you would also generally be expected to file a municipal business tax return. However, many municipalities provide an exemption for the Municipal B&O Tax to come into play. For example, in Seattle that exemption is $100,000, so self-employed individuals with gross annual income below the exemption would not need to pay any municipal B&O tax but would still need to file a municipal business income tax return.

Hawaii: Aloha General Excise Tax for Self-Employed and Renters

The Aloha State does not have local income taxes per se, but most self-employed individuals are required to register for and file the Hawaii General Excise Tax, which is often equated with a sales tax, as it can be passed on to the final consumer (although final liability for its payment lies with the business or self-employed individual).

Note that unlike sales taxes in other states, most services are subject to the Hawaii General Excise Tax. Also, unlike the New Mexico Gross Receipts Tax (which, in many ways is very similar to the General Excise Tax), Hawaii also classifies rental income (reported on Federal Form 1040, Schedule E) as income subject to the General Excise Tax). Hawaii counties may also impose a County General Excise Tax surcharge. A 0.5% surcharge is currently imposed in Honolulu, Kauai, Hawaii, and Maui counties (there is currently no surcharge in the remote Kalawao County). The Hawaii General Excise Tax and county surtaxes are paid to the State of Hawaii on State Form G-45 (note that you would first need to register your business and obtain a Hawaii Tax ID by filing Form BB-1).